During the October 1, 2013 to December 31, 2013 review period, we analyzed over five hundred SEC comment letters related to Form 10-K and Form 10-Q issued to companies with a market capitalization between $100 million and $1billion. The result of our review generated consistent results with our previous analysis as MD&A, Revenue Recognition, Taxes and Compensation continue to be areas of focus.

Our analysis included 20 SEC comment letters related to Form S-1, which has been a particular area of focus during the fourth quarter of 2013 as result of the surge in initial public offerings (IPOs). There were 178 IPOs during 2013, which is the highest number of IPOs since 2004, and Emerging Growth Company (EGC) status offerings accounted for 82% of all filings.1

EMERGING GROWTH COMPANIES

EGC status was created in the Jumpstart Our Business Act (the “JOBS Act”), enacted on April 5, 2012, to provide a streamlined path to access capital for companies with less than $1 billion in total revenue during its most recently completed fiscal year. The scaled down IPO disclosure requirements include:

- Two years of audited financial statements and selected financial data;

- Management attestation on internal control over financial reporting starting with the second Form 10-K, without a requirement for an auditor attestation report;

- Compensation disclosure reductions to include executive compensation disclosures on three named executive officers instead of five and no compensation discussion and analysis section, to name a few;

- New accounting standards to be adopted concurrent with private company effective dates;

- Confidential nonpublic reviews of draft IPO registration statements by the SEC staff, provided that the initial confidential submission and all amendments are publicly filed with the SEC no later than 21 days before the IPO “road show”.

CFGI’s analysis included 20 S-1 filings during the fourth quarter of 2013. SEC staff comments on filings under EGC status have asked for additional disclosures on the prospectus cover page to identify the Company as an EGC filer, a summary of the various exemptions and elections available to an EGC and a description of the circumstances and timing that a company may lose EGC status. Additional findings are detailed below.

RESULTS OF ANALYSIS

Through our review of S-1 filings, we identified the following key accounting and reporting considerations for companies expecting to file for the first time with the SEC:

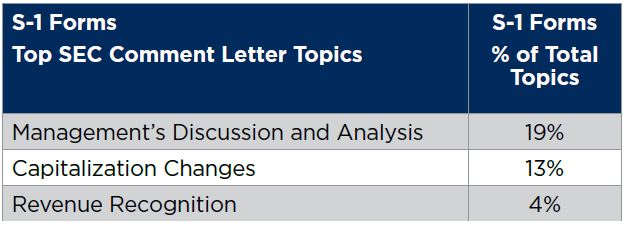

MANAGEMENT’S DISCUSSION AND ANALYSIS

Similar to other filings, SEC staff comments on IPO registration statements are focused on MD&A. The SEC staff frequently requests additional clarifying language to help investors understand the registrant’s business since the facts and circumstances surrounding these company profiles are being introduced to investors for the first time. For instance, in the executive overview section, registrants may receive a SEC staff comment for details on how the size of a market was calculated and additional details on the customer segmentation and competitors within that market. Another continued focus is to ensure your company’s relevant reporting and disclosures within MD&A are adequate and thorough by describing the underlying factors that drive the business.

REVENUE RECOGNITION

SEC staff comments on IPO registration statements focus on revenue recognition due to the importance and complexity of revenue recognition models. Areas of focus continue to include multiple-element arrangements, software revenue recognition, milestone arrangements, proportional performance models, collaboration arrangements and sales incentive programs.

SEC staff comments are aimed at providing investors with disclosures on the substance and fact pattern of the rights and obligations within revenue arrangements and on the significant assumptions used and judgments made in the timing and amounts of recognition.

It is important that your company includes in its S-1 filing a clear and concise description of its revenue transactions as well as a complete description of the significant conclusions reached in the accounting model used to recognize those transactions.

CAPITALIZATION CHANGES

Changes in capitalization that occur simultaneously with the closing of an IPO is a common area subject to SEC staff comments due to the significant complexities involved with capitalization transactions. Typically, a pro forma balance sheet that reflects capital activity must be included in the filing to show the impact of the adjusted capital structure resulting from the IPO. Such capitalization changes may include the automatic conversion or redemption of preferred stock into common stock, the conversion of convertible debt into common stock or the reclassification of warrants to purchase convertible preferred stock from debt to equity. An example of a SEC staff comment follows:

“Please revise your pro forma balance sheet and earnings per share to give effect to this change in capital structure and revise the notes to the pro forma financial information to explain the nature and terms of this change in capital structure. The notes to your pro forma financial statements should also explain how any changes in weighted average shares outstanding were calculated or determined.”

This example illustrates the depth of knowledge required to prepare a pro forma balance sheet for an IPO transaction as well as the necessity for your company to perform a holistic review of its capital structure to ensure the pro forma balance sheet is appropriately adjusted.

KEY CONSIDERATIONS

EGC filing status provides streamlined regulations when entering public capital markets. Preparing an IPO registration statement offers unique challenges in comparison to other filings as it marks the company’s public introduction to investors. Preparing an IPO registration statement also offers some similar challenges, for instance, MD&A and revenue recognition are also top SEC comment letter topics for all filings and; therefore, require particular emphasis from all companies. Knowing the SEC focus areas and observing best practices in the preparation of your S-1 filing will reduce the likelihood of receiving SEC comment letters.

1 Wilmer Hale 2013 Year-End IPO Market Review, January 29, 2014