The Financial Accounting Standards Board, through the Joint Transition Resources Group for Revenue Recognition (TRG), continues to address challenges identified in implementing and applying the new revenue standard. Most recently, the FASB issued three new Accounting Standard Updates (ASU) to address questions discussed by the TRG across a handful of different areas.

In this CFGInsight, we look at the following updates made in these new ASUs:

- Principal vs. Agent Determination

- Identification of Performance Obligation

- Licensing

- Other Narrow Scope Improvements

ASU 2016-08, Principal versus Agent Considerations (Reporting Revenue Gross versus Net)

On March 17, 2016, the FASB issued clarifying guidance for the principal versus agent guidance considerations under the new revenue standard in response to comments received by the TRG as well as providing additional examples to aid in assessments.

The update discusses the level at which the principal versus agent determination should be made, specifying that for each distinct good or service promised to the customer, a company must determine whether it is the principal or the agent. Under a single contract, a company could be a principal for some promises and an agent for others.

The new guidance provides additional clarity on how to apply the control principle when a third party is involved. A company is the principal if it obtains control of a good from the third party and then transfers it to the customer; has the ability to direct the third party to provide a service to the customer on the company’s behalf; or receives a good or service from the third party and combines it with other goods or services to provide to the customer.

The guidance emphasizes that the purpose of the five indicators to determine whether a company is a principal is to support or assist in the assessment of control. The indicators may be more or less relevant to the control assessment, and one or more indicators may be more or less persuasive to the control assessment, depending on the facts and circumstances. This change from the current guidance eliminated strong indicators that led to gross or net presentation.

ASU 2016-10, Identifying Performance Obligations and Licensing

On April 14, 2016, the FASB issued guidance for identifying performance obligations and accounting for licenses of intellectual property (IP).

Performance Obligations

In response to questions discussed by the TRG, clarification was added to aid entities in assessing when promised goods or services are considered separately identifiable and thus treated as separate performance obligations. The new guidance emphasizes that the complete contract versus the individual promise should be evaluated when considering the ‘distinct in the context of the arrangement’ criterion and adds three indicators to perform this assessment. Additionally, new interpretive examples were added to emphasize the new guidance.

The update also introduced language aimed at reducing the cost and complexity of identifying performance obligations by allowing entities to disregard promised goods and services that are deemed immaterial in the context of the contract. Additionally, companies are permitted to account for shipping and handling costs incurred after control of the goods has been transferred to the customer as an expense rather than an additional promised service.

Licenses of IP

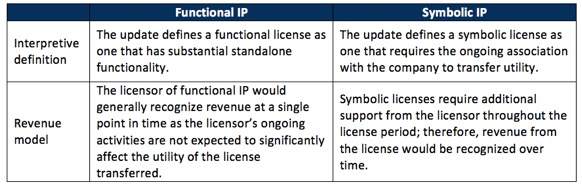

The revised guidance clarifies how companies should determine the nature of their promise when granting IP licenses. The nature of that promise drives the revenue recognition pattern. Companies need to classify IP as either ‘functional’ or ‘symbolic’ based on whether or not the IP has standalone functionality.

Further guidance is introduced on sales- and usage-based royalties made in exchange for IP licenses that dictates a company should recognize revenue at the later of 1) the subsequent sale or usage, or 2) the point in time when the performance obligation tied to the royalty has been satisfied. The TRG had received interpretative questions on splitting royalties which have been dismissed and the TRG has instructed companies to apply royalty guidance to transactions that only involve licensing IP, or where licensing IP is the predominant item for which the royalty relates.

ASU 2016-12, Narrow-Scope Improvements and Practical Expedients

On May 9, 2016, the FASB issued guidance to provide narrow-scope improvements and practical expedients. This amends the new revenue recognition guidance on customer contracts at transition, customer collectability assessment, noncash consideration, and the presentation of sales taxes and other similar taxes collected from customers.

Completed Contracts: The update provides clarifying guidance that, for purposes of transition, a completed contract is one for which substantially all revenue has been recognized under legacy GAAP. Additionally, companies will be permitted to apply the modified retrospective transition approach either to all contracts or to completed contracts only.

Contract Modifications: The update provides companies with a practical expedient to determine and allocate the transaction price based on all satisfied and unsatisfied performance obligations in a modified contract as of the beginning of the earliest period presented under the new standard.

Disclosure: The update clarifies that retrospective adoption of the standard does not require an entity to disclose the effect of the accounting change for the period of adoption. However, the effect of changes on prior periods retrospectively adjusted is required to be disclosed.

Assessing Collectability: The update clarifies the objective of the collectability criterion in Step 1. The objective of collectability is to determine whether the customer has the ability and intention to pay for the promised goods or services. Additionally, a new criterion was added to clarify when revenue would be recognized for a contract that fails to meet the criteria in Step 1. Upon failure of Step 1, companies may recognize revenue equal to the nonrefundable consideration received once control of all goods or services has been transferred to the customer and the company has no further obligation to transfer additional goods or services.

Noncash Consideration: The update specifies that the fair value of noncash consideration is to be measured at contract inception. This is a change where now, most typically, fair value measurement would be done at the time the performance deliverable is complete.

Presentation of Sales Tax: The update allows companies to make an accounting policy election to exclude sales (and similar) tax collected on behalf of third parties from the transaction price.

Next Step on Path to Adopting the New Standard

Through the TRG, the FASB continues to offer amendments, interpretative examples and clarification to the new standard. These TRG updates are aiding companies as they prepare to adopt the new standard. January 1, 2016 marks the beginning of the earliest comparative period for calendar year-end public companies applying the full retrospective adoption method. At CFGI, we are working closely with our clients to identify, assess and document the impact of the new guidance as well as any related systems, processes and controls changes that may be required. Let our experience assisting clients across a variety of industries help your company in its adoption of the new guidance. Please contact us for more information.