As part of our series on current trends with SEC Reporting, CFGI analyzed over 100 comment letters made available by the SEC between April 1, 2013 and September 30, 2013. The focus of our analysis related to the Financial Statements, footnotes and related disclosures made in Management’s Discussion & Analysis filed on Form 10-Q and Form 10-K of companies with a market capitalization between $100 million and $1 billion.

Key trends identified indicate consistency among the areas receiving comments when compared to CFGI’s prior comment letter analysis, which covered the period from January 1, 2013 to March 31, 2013. Our analysis found several key accounting and reporting considerations that registrants should consider in their upcoming filings.

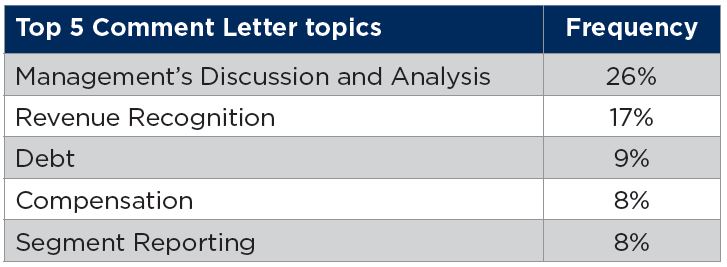

MANAGEMENT’S DISCUSSION AND ANALYSIS.

Comments requesting registrants enhance the discussion of underlying reasons for certain changes or emerging trends in a company’s business operations continue to be a theme. The SEC staff is looking for registrants to more fully disclose why significant changes occurred by identifying specific drivers of the change to operations in the period. An example of a SEC staff comment follows:

“Please provide a more detailed analysis of the reasons underlying each material quantitative change in operating measures from period to period. For example, fully explain the significant decrease in income from operations attributable to the ABC segment in fiscal 2012. Your discussion should explain the cause of underlying factors which led to material shifts, rather than simply listing factors such as decreased enrollments and higher operating costs. Where acquisitions materially impact financial line item shifts, please quantify that impact. For example, quantify the impact the acquisition of XYZ had on ABC revenues. Finally, more fully explain disproportionate line item shifts.”

This example highlights the theme of many of the comments issued in this area, which is a continued focus by the SEC on the depth and quality of the analysis provided by registrants.

REVENUE RECOGNITION

The SEC staff’s continued focus on revenue recognition disclosures aims to assist the financial statement user in gaining a deeper understanding of registrants’ revenue recognition models. Areas of focus include milestone arrangements, proportional performance models, contingent consideration, extended payment plans with customers, warranty obligations and sales return reserves. These areas require significant judgment and the SEC staff’s goal with their comments is to ensure registrants’ patterns of revenue recognition are clearly understandable based on the disclosures in these filings.

DEBT

The SEC staff has looked closely at registrants for debt modifications and restructurings. The SEC staff has requested enhanced disclosures regarding gains and losses recorded on extinguishment of debt as well as the accounting for deferred financing costs related to the original debt.

COMPENSATION PROGRAMS

The SEC staff comments have been focused on adequately describing factors that impact variable compensation plans including the description metrics assessed on performance tied plans and the assumptions used to establish the value of compensation programs. An SEC staff comment to a registrant that has a cash bonus award plan is as follows:

“Please advise whether the decision to award cash bonuses is purely discretionary or is triggered by the achievement of performance targets, such as revenue and operating income”.

In addition to focusing on providing the financial statement reader with sufficient information to understand the significant compensation programs of the registrant, registrants need to ensure consistency between Financial Statement footnote disclosures and disclosures contained in the Compensation Discussion and Analysis disclosures.

SEGMENT REPORTING

The SEC staff showed a consistent theme of requesting that registrants discuss the qualitative and quantitative factors considered when aggregating product lines and/or reporting units into a single operating segment in accordance with the characteristics established by Accounting Standards

Codification (“ASC”) Topic 280. Additionally, the Staff inquired about changes to the Chief Operating Decision Maker (CODM), as registrants experienced significant business changes including significant organic growth as well as acquisitions.

RESPONSE CONSIDERATIONS

The SEC’s focus continues to be on the depth, completeness and adequacy of disclosures. To minimize the burden and likelihood of receiving follow-up comments, consider the following strategies:

- Pay particular attention to these SEC focus areas and ensure your company’s relevant reporting and disclosures are adequate and thorough. The SEC’s National Conference on Current SEC & PCAOB developments is scheduled for the week of December 9, 2013, which typically produces a “Frequent Areas of Comment” presentation. Focus areas noted at the 2012 conference were consistent with the top 5 comment letter topics noted in our independent analysis;

- Anticipate potential SEC comments about key judgments and be ready to answer questions before they come by preparing internal documentation in a manner that can be easily converted into a formal response to a comment letter. Companies with an established process to document key judgments contemporaneously with their filings will benefit if the SEC staff were to comment on that area;

- Track recent SEC releases and other resources to keep your organization abreast of the latest guidance; and

- Identify an internal plan for comment letter response, including resources that will assist when comment letters are received as a typical comment letter provides for a ten day response period.