The IPO is a critical inflection point for your organization, marking a crucial shift in expectations for the business. For finance leaders seeking to influence the way their organizations operate, the period leading up to the IPO is a critical time to make changes. By thinking about the operational impacts of preparing for an IPO – rather than solely considering the regulatory requirements – you stand to save time and money down the road. More preparation today means fewer issues later on.

If your business is planning to go public in the next 24 months, this guide will help you address the operational considerations that ensure your organization’s stability prior to and following the IPO. This guide will examine:

- Considering the upfront implications of Securities and Exchange Commision (SEC) regulations on your business.

- Understanding your current segment structure and making the necessary operating model changes.

- Exploring changes to your reporting expectations and close process.

- Planning to have the people, process and technology to support your desired operating model as a public company.

IPO regulations will affect the way you operate

Too often, companies look at an IPO as a procedure to follow. Hit all the right milestones, and your company will go public and gain all the benefits that come with it. But this often fails to consider the structural changes necessary to ensure success after the IPO. Though it is crucial to file the right paperwork in the correct order, it is also important to make strategic decisions about your organizational and leadership structure, your operating processes that have financial impact, your finance and accounting process, and your technology blueprint at this critical juncture.

Going public means that you will have a whole new set of stakeholders: public investors and the regulatory authorities that support them, requiring greater transparency on the inner workings of the business including business’ segments, products, strategies and locations.

Key considerations

- What are the IPO regulations that will affect your business?

- Are you prepared for those regulations?

- What steps can you take now to get ahead?

What is a segment, and how will that change how you need to operate?

Pre-IPO, your business has been rightly focused on growth; your key stakeholders implicitly understand the way you operate. This comfortable dynamic will change during the IPO, which means you need to think about how your business is organized for success in the future.

Regulators have specific definitions of segments. Generally, an operating segment is a profit center within an entity that has distinct financial data; segments are reviewed by chief decision-makers, who make assessments and define resource allocations. The way you report segments is driven by how you report financial data, the way you have aligned with your leadership structure, and the manner in which your chief decision-makers analyze and manage the business.

Consider the implications segment reporting will have on your business down the road and make the necessary changes to your reporting packages and organizational structure to support your future vision for the company and how you would like to report your financial results. An IPO can be a catalyst for transforming your business for the future, so you should think carefully about how your segments will align with your vision for the future.

Key considerations

- How is my business and operating model structured today?

- Have I thought critically about my operating model for the future?

- What segments do I want to report on?

New expectations for financial close and reporting

When your business goes public, you may need to report your results at a more granular level, including reporting segments, revenue by product, Non-GAAP measures, pro-forma financial information, estimates requiring a high degree of judgement etc. Your organization may not currently have the capacity to automate this type of reporting. Manual manipulation of data may be required to get the reporting information you need.

This point is important because you will need to close, draft financials and go through reviews within 45 days of quarter end. Pre-IPO, you should ask yourself if you are prepared to meet these expectations. Not only will you need to close faster than before, but you should also do so more precisely. Because these financials will be reviewed by auditors likely with a lower risk tolerance, you will need to provide greater assurance that you have mitigated risks such as cut-off issues, incomplete data, potential financial inaccuracies, inaccurate disclosures and/or stale assumptions, particularly in high judgement areas.

Consider investing in updates to your finance/accounting processes and the technology that supports them including in areas like financial data capture, reporting, close cycle and SOX compliance. Not only will this facilitate your close process, but if properly planned for, may also create future cost savings.

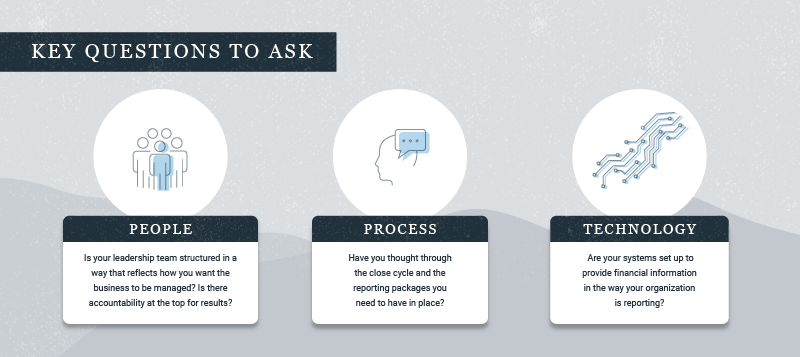

Key questions to ask

- What products do you want to report on?

- What do you not report on today that you will be required to report on in the future?

- Do you have the processes and systems in place to report on these required items?

- What steps do you need to take to close within 45 days of quarter end?

Preparing your people, process and technology for an IPO

The way you report and how you structure your operating model will have significant impacts on your people, process and technology.

It is important to consider the complex interrelationships between these three areas before going public. For example, leaders will need to be accountable for their segments and products. Think carefully about how each team is structured and how it will impact reporting. Do your current systems properly capture and report on the necessary metrics? Have you identified all the information produced by the entity (IPE) to ensure that you have the proper management review controls in place?

Other considerations when going public

Every company is unique and will have a different set of challenges to face when going public. In our experience, here are some representative actions you can take to prepare:

- The S-1 process is extremely labor intensive, and it is best to have a trusted partner guide you through the process.

- During the S-1 process, you will need to choose an underwriter as well as hire external legal securities counsel, a printer and a transfer agent.

- Train your management team to be ready to handle external communications, and build a process to ensure consistent messaging.

- Prepare your organization for the expectations and rigor of public company audits.

- Early growth companies (EGCs) with high growth over the past few years should consider quarterly reporting to show revenue multiples.

- Ensure your accounts payable process is well structured so that you can capture all expenses, including accruals, in a timely manner.

- Consider the impact on your financial close and if you have the bandwidth needed to execute from a people perspective, as well as the processes and technology needed to create an accelerated close.

- Transition your stock compensation from Excel to stock compensation software with proper controls.

- Ensure you are prepared for Sarbanes-Oxley requirements. This is especially applicable to EGCs. You may need to draft procedures and policies that were previously not documented. In addition, you may need to implement controls and test against them.

- For companies with a high number of leases (e.g., healthcare, retail, real estate), prepare for ASC 842 regulatory guidance by considering implementing lease accounting software.

- If you recently acquired a company, consider the impact of S-X 3-05, which will require you to produce pre-acquisition audited financials for each of those companies.

- EGCs should decide whether to take advantage of the one-time election to delay accounting guidance implementation (e.g., ASC 606 – Revenue Recognition). Taking advantage of this opportunity can give organizations the bandwidth to properly implement guidance from an operational perspective.

A partner to your organization

An IPO marks a fundamental change to your business. You need to carefully consider the implications of regulations on your business from people, systems and technology perspectives. Having a plan in place today will greatly benefit your organization in the future.

Our team has end-to-end expertise to assist you with the end IPO process from assistance in preparing financial disclosures for the S-1 process, to helping you establish an appropriate public company control environment, to helping you organize your people, process and technology operations to meet your new challenges.

If you are interested in learning more, please contact Andres Garzon, Partner (agarzon@cfgi.com, 617-306-1888), April Coleman, Partner (acoleman@cfgi.com, 603-686-2020) or Oscar Palacio, Partner (opalacio@cfgi.com, 617-921-3469).